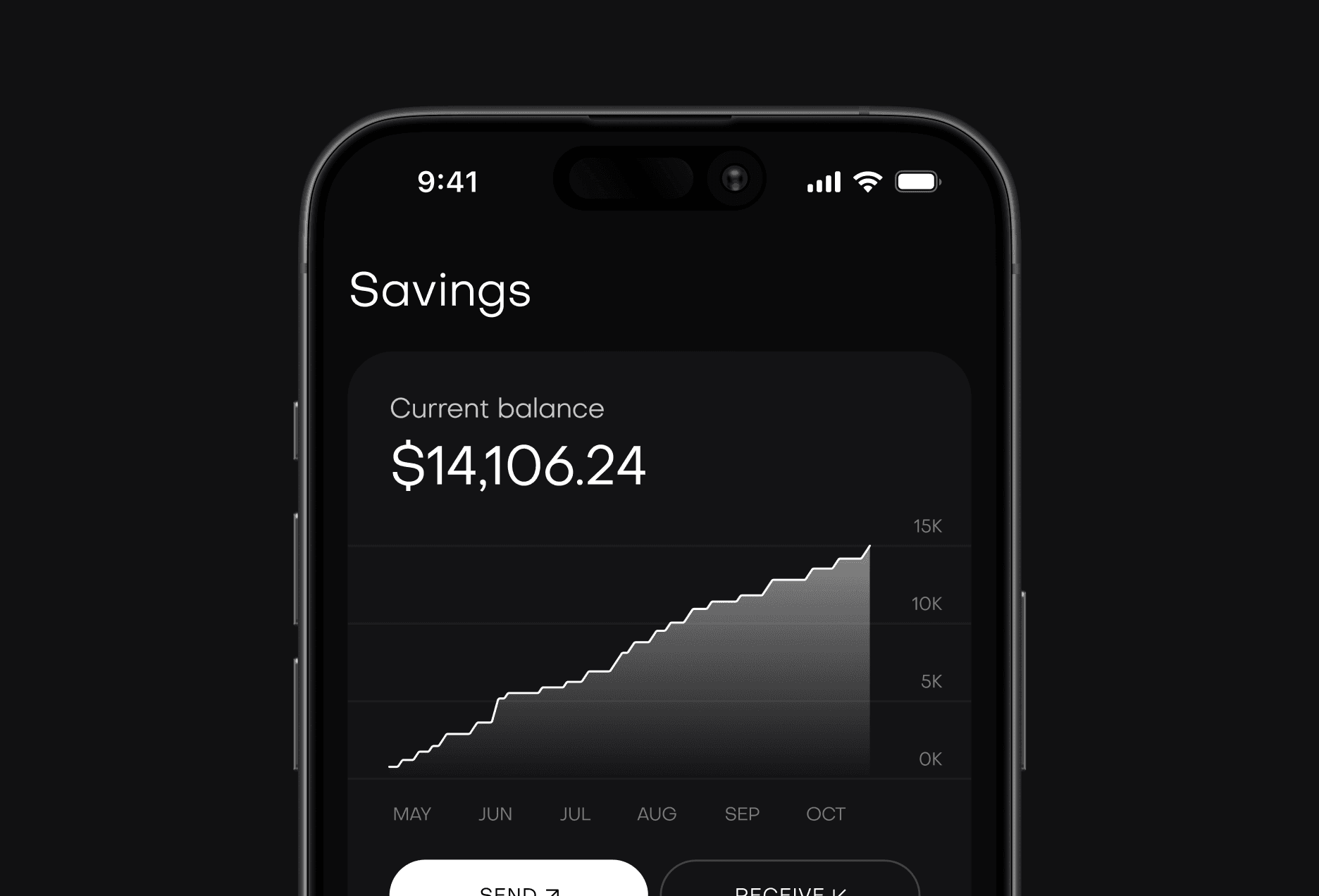

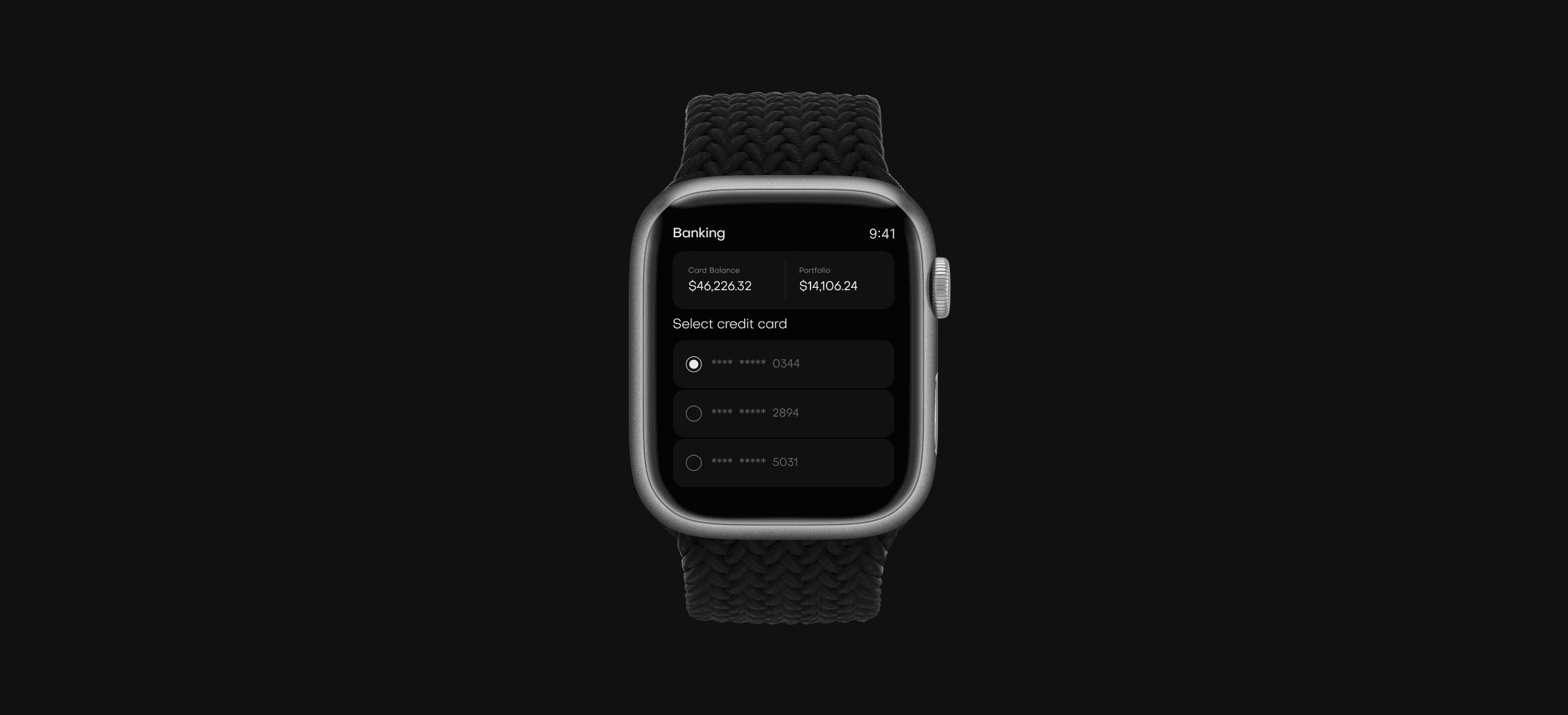

Banking is now available on your wrist: watchOS app is out!

Our new watchOS application is finally here! Manage your finances, check balances, and receive alerts directly from your wrist.

Setting financial goals for different life stages

Establishing clear financial goals is crucial, and these objectives naturally evolve as you move through life. Whether you're starting your career, buying a home, or planning for retirement, your strategy must adapt. This guide outlines how to set achievable financial milestones for every stage.

Common pitfalls to avoid in savings planning

Many well-intentioned savings plans fail due to common errors. Overlooking high-interest debt, failing to automate savings, or not having a clear budget can derail your progress and financial security.

Setting vague or unrealistic savings goals without a plan.

Not creating an emergency fund to cover unexpected life expenses.

Forgetting to account for inflation's impact on savings.

Failing to review and adjust your financial plan regularly.

By recognizing these potential missteps, you can build a more resilient financial strategy. Awareness is the first step toward proactive planning, ensuring your savings efforts are effective and aligned with your long-term ambitions. Regular check-ins help you stay on track and adapt to new challenges.

Now that we have identified what to avoid, let's focus on what to do. Building a solid financial future isn't just about sidestepping mistakes; it is about constructing a strong foundation with proven strategies and clear, actionable guidelines.

Guidelines for savings: Building a strong Foundation

A successful savings plan starts with fundamental principles. This includes automating your contributions, prioritizing high-yield savings accounts, and creating a budget that clearly distinguishes needs from wants. These core actions form the bedrock of sustainable financial health.

"The simplest rule of saving is also the most powerful: pay yourself first. Automating this single step ensures your future is always a priority."

By consistently applying these guidelines, you transform saving from a chore into a habit. This discipline not only grows your wealth but also provides peace of mind, knowing you are prepared for whatever may lie ahead.

Diversifying Your Savings Portfolio

Beyond a standard savings account, consider diversifying into other vehicles. Certificates of Deposit (CDs), money market accounts, or even low-risk investment funds can offer better returns, protecting your capital from inflation while helping it grow more efficiently over time.

Utilize high-yield savings accounts for better returns.

Explore Certificates of Deposit (CDs) for fixed, secure interest rates.

Consider money market accounts for liquidity and growth.

Look into low-risk bonds as part of your portfolio.

Tailoring your savings plan to your life stage

Your financial needs in your 20s are different from your 50s. A younger person might focus on an emergency fund, while someone nearing retirement will prioritize maximizing their pension contributions.

Adapting savings rules to changing economic conditions

Economic shifts like high inflation or interest rate changes demand a flexible savings approach. What works in a stable economy may need adjustment during a downturn. Regularly reassessing your strategy ensures you stay resilient.