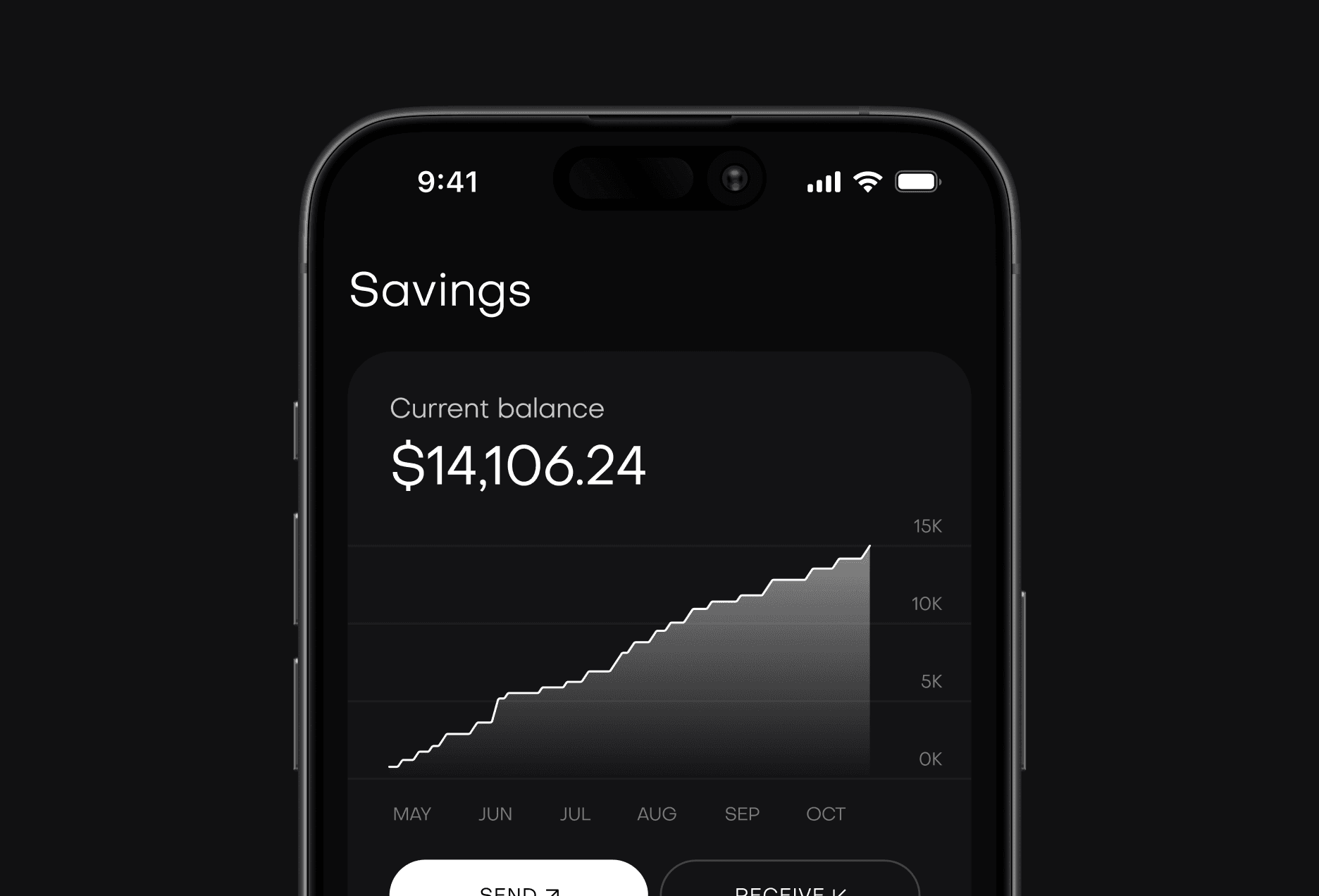

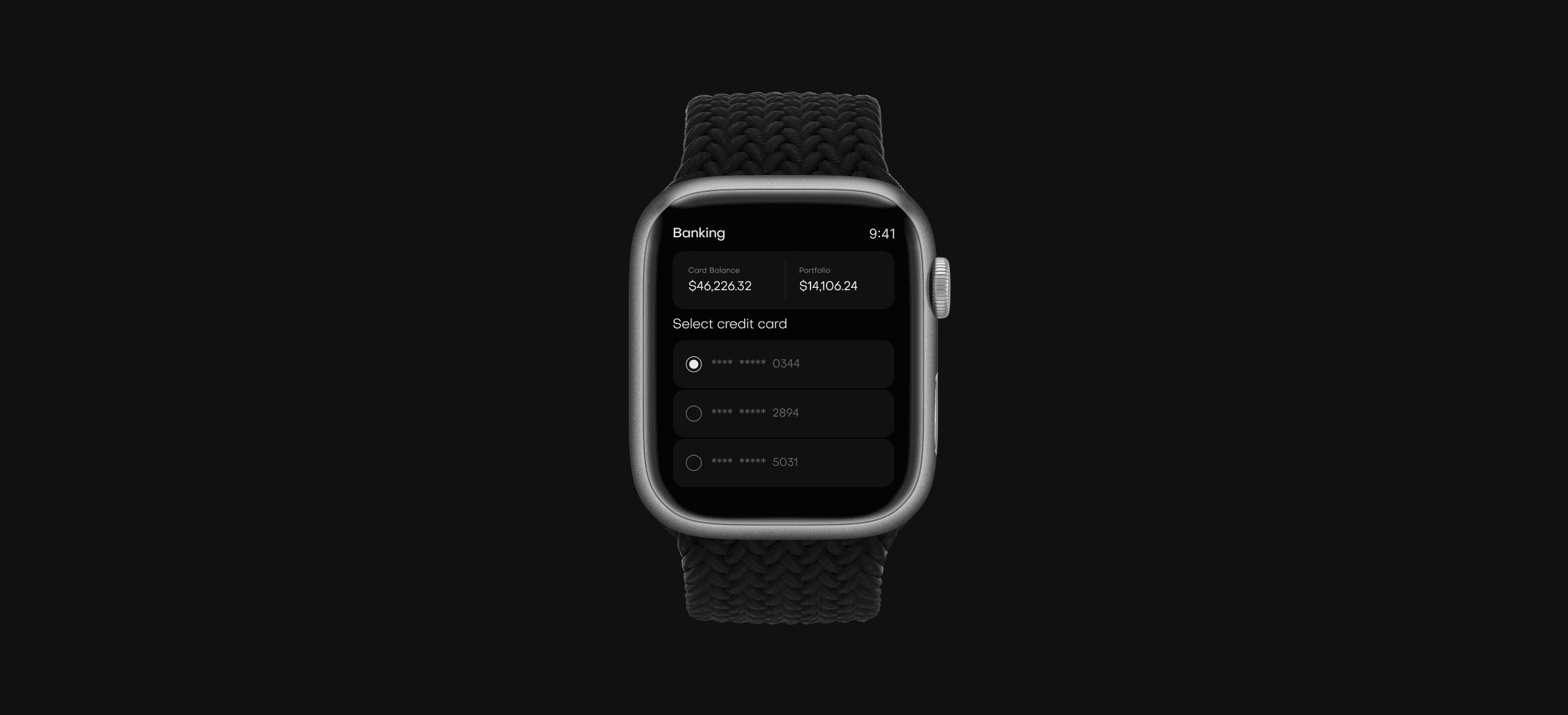

Banking is now available on your wrist: watchOS app is out!

We're thrilled to launch our new watchOS app, bringing seamless banking and account management right to your wrist. Update now to try it.

Setting financial goals for different life stages

Establishing clear financial objectives is crucial as you move through life. Whether saving for a down payment, planning for retirement, or funding education, your goals will evolve. This guide helps you define and adapt your financial strategy for every important milestone.

Common pitfalls to avoid in savings planning

Many people encounter similar obstacles when trying to build their savings. From not having a clear budget to reactive spending, these pitfalls can derail progress. Understanding these common mistakes is the first step to financial success.

Failing to create and stick to a detailed monthly budget.

Overlooking high-interest debt that cancels out your savings gains.

Not automating your savings transfers to make it a priority.

Setting unrealistic goals that lead to early discouragement.

By being aware of these potential setbacks, you can create a more resilient and effective savings plan. It's not just about putting money aside; it’s about creating smart habits that support your long-term financial health. The key is consistency and adjusting your strategy as your life changes.

With those potential issues in mind, let's shift our focus to constructing a successful savings strategy. Building a solid financial future begins with a few core principles that anyone can follow, regardless of their current income or situation.

Guidelines for savings: Building a strong Foundation

Your first step should be establishing an emergency fund that covers 3-6 months of essential living expenses. This provides a crucial safety net. Next, prioritize contributing to retirement accounts to take advantage of compound growth. Finally, set specific, achievable short-term goals.

“A disciplined savings plan is the foundation of financial freedom. It empowers you to handle life's surprises and pursue your dreams.”

Implementing these guidelines requires a clear view of your income and expenditures. Use our online budgeting tools to track where your money goes, identify areas for savings, and monitor your progress toward your financial objectives over time.

Choosing the Right Savings Accounts

Not all savings accounts are created equal. A high-yield savings account offers a better interest rate than a traditional one, allowing your money to grow faster. For long-term goals like retirement, consider exploring investment options that align with your risk tolerance.

Research accounts with the highest Annual Percentage Yield.

Check for monthly maintenance fees or minimum balance requirements.

Consider online banks, as they often offer better rates.

Look for FDIC insurance to ensure your funds are protected.

Tailoring your savings plan to your life stage

A recent graduate's savings plan will look very different from someone nearing retirement. Early in your career, focus on building an emergency fund. Later, you can shift focus to maximizing retirement contributions.

Adapting savings rules to changing economic conditions

Economic shifts, like inflation or interest rate changes, can impact your savings. It's wise to review your plan annually. During high inflation, you may need to increase contributions to meet goals. In a recession, preserving your emergency fund becomes paramount.