9 great productivity apps you can download for free now

Explore our top picks for free productivity apps designed to boost your workflow and help you get more done, starting today.

Setting financial goals for different life stages

Setting clear financial goals is crucial as you move through life. Whether you're just starting your career, buying a home, or planning for retirement, your objectives will shift. This guide helps you tailor your financial strategy to your current and future needs for lasting success.

Common pitfalls to avoid in savings planning

Many people struggle with saving due to common mistakes. These can include not having a specific goal, ignoring inflation, or failing to automate contributions. Understanding these pitfalls is the first step to building a resilient savings plan.

Setting vague goals like "saving more" without a target amount.

Forgetting to adjust your savings plan after major life events happen.

Dipping into long-term savings for short-term, impulsive wants.

Ignoring the power of compound interest by starting too late.

By being aware of these common errors, you can proactively build a more effective financial strategy. It's not just about avoiding mistakes, but about creating positive habits that lead to sustainable growth. Let's look at how you can apply these principles to build a solid foundation for your financial future.

Avoiding these issues requires discipline and a clear plan. Regularly review your financial situation and adjust your strategy as needed. The key is to stay informed and committed to your goals, turning potential setbacks into opportunities for strengthening your financial literacy.

Guidelines for savings: Building a strong Foundation

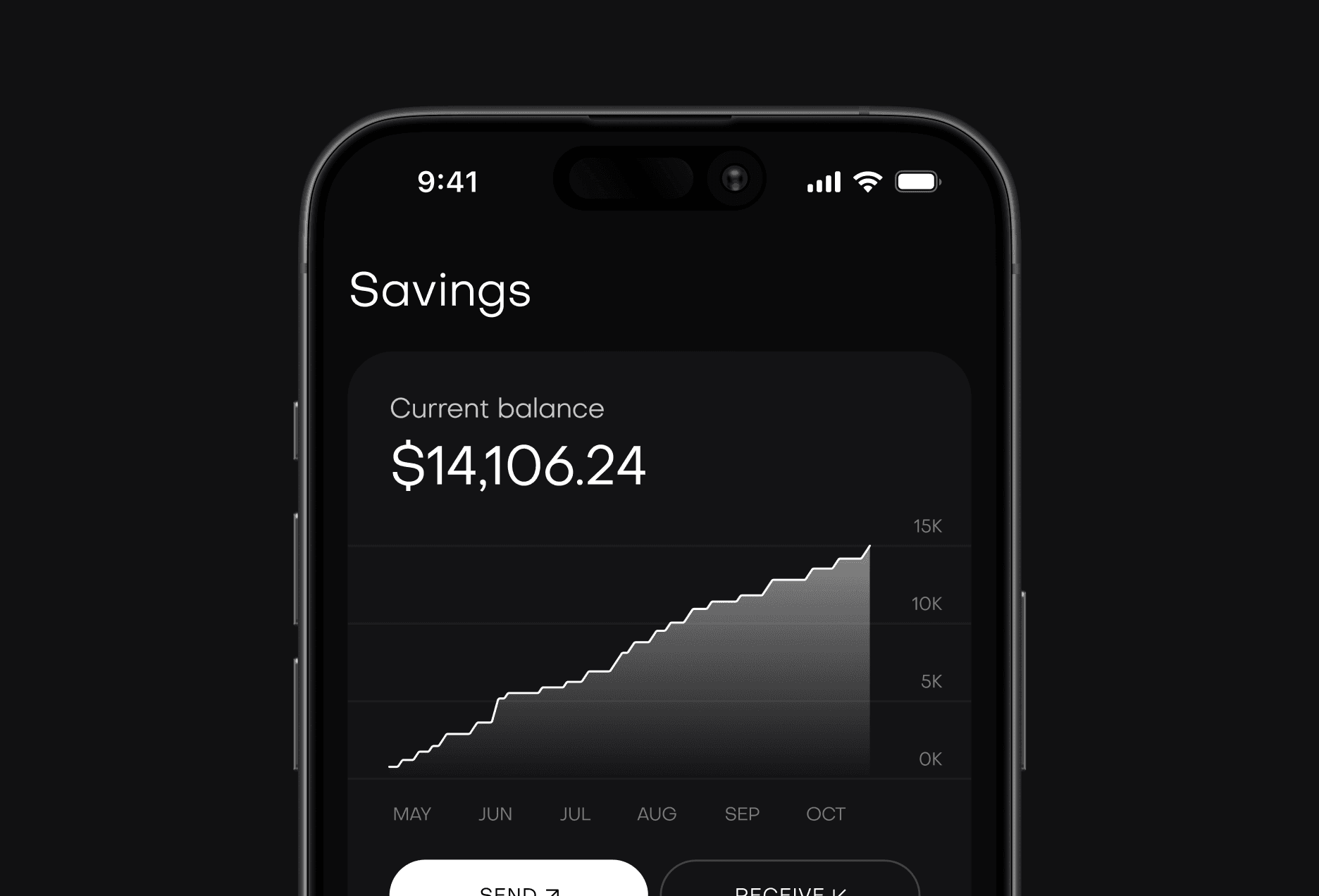

To build a robust savings foundation, start with the basics. A well-defined budget is your roadmap, outlining your income and expenses. From there, you can establish an emergency fund to cover unexpected costs without derailing your long-term objectives. This creates a safety net.

"A solid financial plan is a blueprint for your future. It's the essential first step towards achieving security and independence."

Once your emergency fund is established, focus on consistent contributions to savings and investment accounts. Automating transfers can help you build wealth effortlessly over time, making your financial foundation even stronger.

Automating Contributions for Consistent Growth

Setting up automatic transfers from your checking to your savings account is a powerful strategy. It removes the temptation to spend and ensures you're consistently working toward your goals. This 'pay yourself first' approach is a cornerstone of disciplined financial planning.

Schedule your automatic transfers to align with your payday.

Start with a small amount and gradually increase it as you get paid.

Use a high-yield savings account to maximize your growth.

Split your direct deposit between checking and savings.

Tailoring your savings plan to your life stage

Your financial priorities in your 20s, like paying off student loans, will differ from your 50s, when retirement is closer. It's vital to adapt your savings strategy to match your age and specific life goals.

Adapting savings rules to changing economic conditions

Economic shifts like inflation or interest rate changes can impact your savings. A flexible plan allows you to adjust. During high inflation, you might prioritize investments that outpace it, while low rates could favor different strategies.